Algorithms, DOGE, Investigations and Lawsuit:The Highly Debated Yet Poorly Understood Federal Government Payment System

Context

Government payments—whether for grants, salaries, or contracts—follow a strict pathway to protect public funds and ensure accountability. This process has been the backbone of federal financial management. However, recent policy changes, including creating the Department of Government Efficiency (DOGE) by executive order, have introduced new dynamics.

A recent lawsuit against DOGE’s intervention in the Bureau of the Fiscal Service, a Department of the Treasury component, has sparked a debate over the balance between the new presidential policies and statutory mandates in government operations. This follows, two government watchdogs—Treasury's acting inspector general and the Government Accountability Office—have begun investigations into Treasury Secretary Scott Bessent’s decision to grant DOGE access to federal payment systems. The issues include gaining access to the Treasury’s financial systems by political appointees, Special Government Employees, or anyone detailed to the Treasury from elsewhere and the risk of disclosing sensitive and private information. When examining the whole process related to the lawsuit, investigations, and DOGE's involvement, it becomes evident that the key element lies within the financial mechanics of the process. For example, from a macro perspective, the Bureau of the Fiscal Service (BFS) procedure is to receive payment files from a given agency, process them, and transmit them to the Federal Reserve for final disbursement. It emerges as the critical element.

Furthermore, the Bureau manages the government’s accounting, central payment systems, and public debt and serves as the central payment clearinghouse for most payments to and from federal agencies. BFS’s payment systems include, among others, the Payment Automation Manager (“PAM”) System, which is the federal government’s largest system for receiving payment files and processing payments; the Secure Payment System (“SPS”), through which paying agencies securely create, certify, and submit payment files to Treasury; the Automated Standard Application for Payments (“ASAP”), an electronic payment and information system initiated by recipients; and the Central Accounting and Reporting System (“CARS”), which federal agencies utilize to account for their spending.

While this mechanism may appear straightforward compared to the broader legal aspects of the lawsuit, it underpins the actual flow of funds and has significant implications for all parties involved. Understanding the particulars of this process—the potential for delays, points of control, and the technological infrastructure and algorithms that support it—could prove invaluable in navigating the complexities of the lawsuit and anticipating the potential policy outcomes for DOGE and other stakeholders.

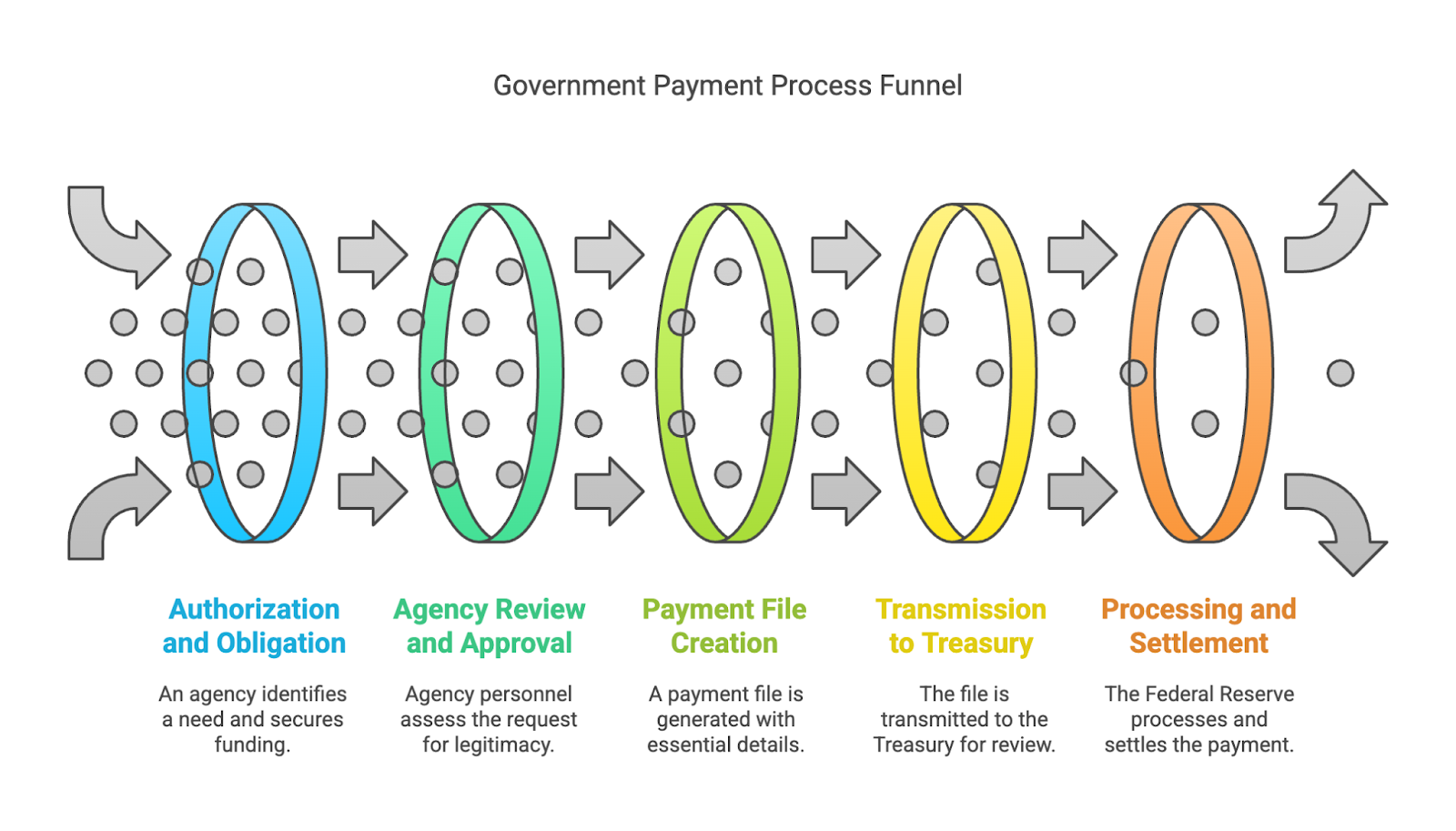

The Payment Process Macro Perspective

The figure above shows that government payments regularly move through several key stages. Each stage includes multiple layers (not shown) of review to maintain transparency, accuracy, and security.

Authorization and Obligation:

An agency identifies a need and secures the necessary funding. Once approved, the agency formally commits to the expenditure—an action known as “obligation.”Payment Request and Submission:

The designated recipient—whether a contractor, grantee, or employee—submits a payment request and supporting documentation that justifies the expenditure.Agency Review and Approval:

Agency personnel rigorously assess the request to verify the legitimacy of the expense, ensure compliance with regulations, and confirm the accuracy of the details.Payment File Creation:

After approval, a payment file is generated containing essential information such as the recipient’s bank details, the amount, and a description of the expenditure.Transmission to the Treasury Fiscal Service:

This file is transmitted to the Bureau of the Fiscal Service within the U.S. Department of the Treasury, serving as a critical checkpoint.Treasury Fiscal Service Verification:

The Fiscal Service reviews the file for technical accuracy and compliance with formatting standards. Their role is to ensure the payment instructions are sound, not to reapprove the underlying expenditure.Transmission to the Federal Reserve:

Once verified, the file is forwarded to the Federal Reserve, which acts as the government’s fiscal agent.Processing and Settlement:

The Federal Reserve processes the payment by debiting the Treasury’s account and crediting the recipient’s account via established systems (such as Fedwire or ACH).Funds Disbursement:

The recipient’s bank posts the funds, making the money available for use.Reconciliation and Reporting:

Finally, the agency, Treasury, and recipient reconcile their records. Often, recipients must submit reports on how the funds were used, ensuring ongoing accountability.

An Example: Department of Education Grant

To illustrate, consider a grant awarded by the Department of Education to a school:

Award and Obligation:

The Department awards a grant for a specific educational initiative and obligates the necessary funds.Payment Request Submission:

After incurring eligible expenses, supported by invoices and receipts, the school submits a payment request to the Department.Review and Verification:

Department staff verify that the expenses comply with grant terms and that all documentation is in order.Payment File Creation and Transmission:

Once approved, a payment file is created and sent to the Treasury Fiscal Service, initiating the process of transferring funds.Federal Reserve Processing:

After verification, the Federal Reserve processes the payment, crediting the school’s bank account.Post-Disbursement Reporting:

The school may be required to report on fund usage, closing the loop on accountability.

The Role of DOGE and the Recent Lawsuit

The recently established Department of Government Efficiency (DOGE) was created by executive order to streamline administrative processes and reduce costs across federal agencies. DOGE’s mandate includes reducing bureaucratic delays and introducing modern management practices within traditional systems.

However, DOGE’s active involvement in the payment process—particularly its interactions with the Treasury Department—has come under legal scrutiny. The lawsuit contends that:

Statutory Overreach:

Critics argue that DOGE’s intervention in Treasury operations may bypass established statutory mandates governing federal financial transactions, potentially undermining longstanding checks and balances.Transparency and Accountability:

The case raises concerns about whether DOGE's new efficiencies might compromise the transparency and accountability embedded in the traditional payment process.Balancing Reform and Regulation:

While modernizing government operations is essential, the lawsuit highlights the challenge of integrating innovative practices with the rigorous standards required by law. Stakeholders call for a careful reassessment of DOGE’s role to ensure that efficiency gains do not sacrifice fiscal responsibility.

The outcome of this legal challenge is expected to have far-reaching implications, potentially redefining how emerging administrative reforms interact with established financial systems.

Conclusion

A series of robust checks and balances support the government payment system—from initial authorization to final disbursement. Integrating reform initiatives like the Department of Government Efficiency (DOGE) represents a significant step toward modernizing federal operations. However, the recent lawsuits and investigations highlight the complexities of such integration, challenging policymakers to find a balance between innovation and the preservation of statutory integrity. As this legal debate unfolds, ensuring that efforts to streamline processes do not compromise the transparency and accountability essential to managing public funds remains crucial.

References

U.S. Department of the Treasury, Bureau of the Fiscal Service. Retrieved from https://fiscal.treasury.gov

Federal Reserve System. Retrieved from https://federalreserve.gov

Government Accountability Office (GAO) Reports on Federal Financial Management.

Executive Order Establishing the Department of Government Efficiency, January 20, 2025: https://www.whitehouse.gov/presidential-actions/2025/01/establishing-and-implementing-the-presidents-department-of-government-efficiency/ and:

Implementing The President’s “Department of Government Efficiency” Workforce Optimization Initiative, February 11, 2025:https://www.whitehouse.gov/presidential-actions/2025/02/implementing-the-presidents-department-of-government-efficiency-workforce-optimization-initiative/

Johnson, M. (2025). “Lawsuit Questions the Role of the Department of Government Efficiency in Treasury Operations.” Government Reform Journal, 18(2), 45–59.

Smith, J. (2025). Balancing Innovation and Regulation: The Future of Federal Payment Processes. Journal of Public Administration.

Defendant's Memorandum of Law in Opposition to Plaintiffs' Motion for a Preliminary Injunction, February 11, 2025: https://storage.courtlistener.com/recap/gov.uscourts.nysd.636609/gov.uscourts.nysd.636609.35.0.pdf

Watchdogs probe DOGE’s access to Treasury payments system, Musk’s fraud allegations, February 14, 2025: https://www.politico.com/news/2025/02/14/gao-doge-treasury-payment-system-00204285?utm_source=chatgpt.com

Comentarios

Publicar un comentario